Are you still carrying a student loan that has been in deferment for 10, 15, or even 20 years? Does checking your balance feel like looking at a bad ex you just can’t get rid of?

For years, we’ve been told that federal student loans are impossible to get rid of. But there has been a major shift. Updated bankruptcy guidelines now allow student loans to be treated much like other types of debt, creating a unique opportunity for borrowers.

If you are struggling with student loan debt, this might be the most important article you read this year.

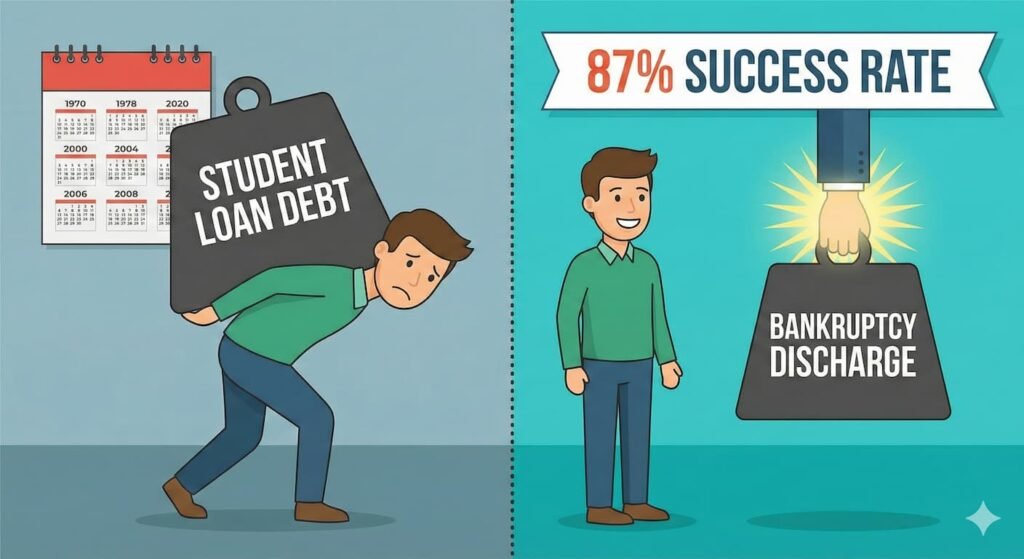

The Bankruptcy Myth: 87% Success Rate

Most people assume that a student loan bankruptcy discharge is a lost cause. However, recent research suggests that 87% of people who actually attempt to discharge their student debt in bankruptcy are successful.

Whether you are filing for Chapter 7 or Chapter 13, the courts are looking at these cases differently now. If paying your student loans would cause “undue hardship”—essentially ruining your financial life—you can ask a judge to erase them. This is the bankruptcy student loan discharge path, and it is a major move that many borrowers are sleeping on.

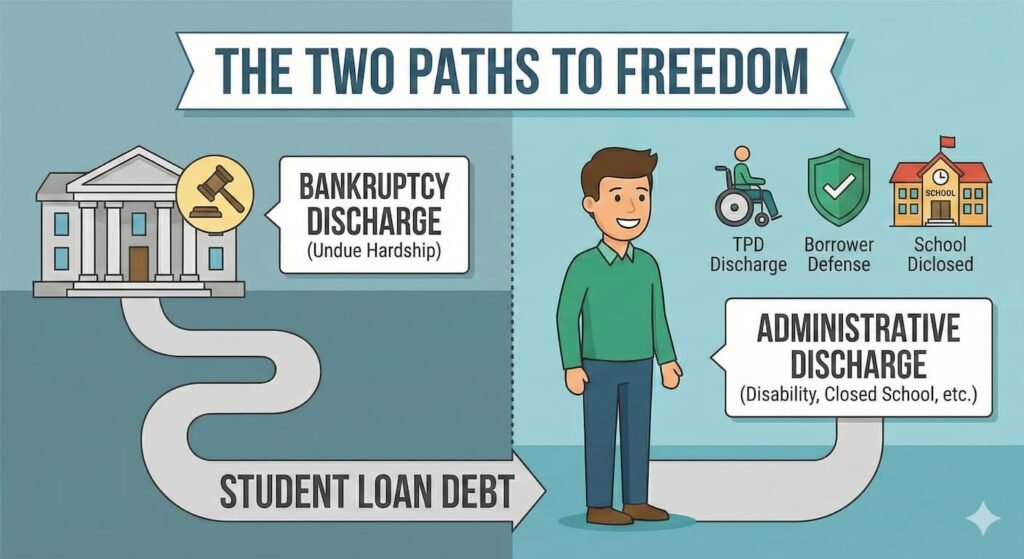

The Two Paths to Freedom

As discussed in our latest video, there are generally two ways to tackle this:

- The Bankruptcy Way: Proving undue hardship in court.

- The Non-Bankruptcy Way: Qualifying for administrative discharge programs.

While bankruptcy is a powerful tool, you should also be aware of other discharge types that might apply to you without going to court:

- Total and Permanent Disability Discharge (TPD Discharge): If you are unable to work due to a disability, you might qualify for disability student loan discharge. This is often coordinated through Social Security or VA documentation.

- Borrower Defense Discharge: If your school misled you or violated state laws, you could be eligible for borrower defense loan discharge.

- Closed School Discharge: If your school is no longer operational (a crucial thing to check!), you might not have to pay that debt back.

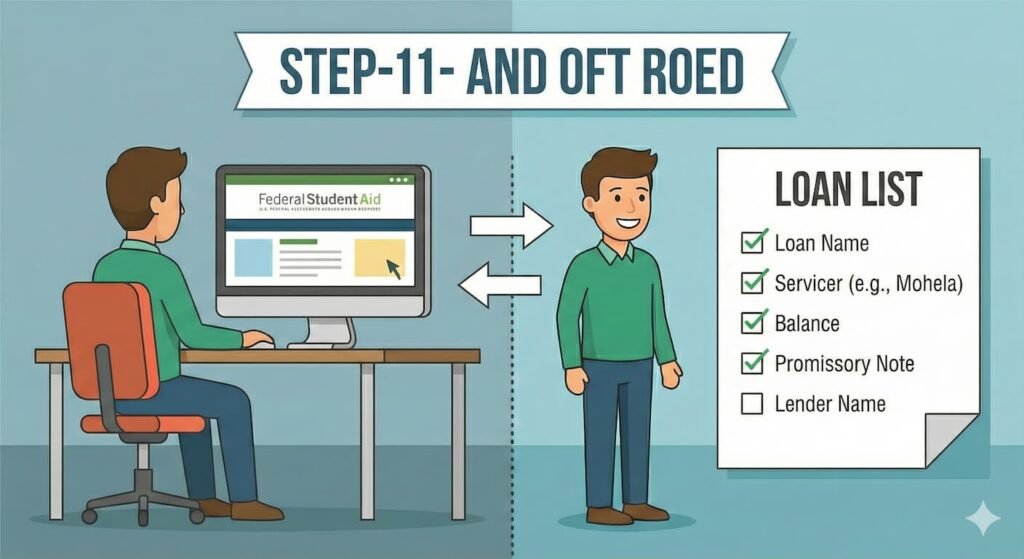

Step-by-Step: How to Discharge Student Loans

Before you file for student loan forgiveness or bankruptcy, you need to get organized. You cannot fight what you don’t understand.

1. Locate Your Loans

Log into your Federal Student Aid dashboard (using your FAFSA login details). You need to know exactly who holds your debt. Is it Mohela? Nelnet? Aidvantage?

2. Create a “Loan List”

Break down every single loan you have. Create a list that includes:

- Loan Name & Servicer (e.g., Nelnet student loan discharge department, etc.)

- Balance & Interest Rate

- Promissory Note (Try to get a copy of this)

- Lender Name (Vital for private loans)

Put them in boxes: Federal Student Loans vs. Private Loans. This full accounting history is required whether you are applying for a student loan discharge application for disability or preparing for bankruptcy.

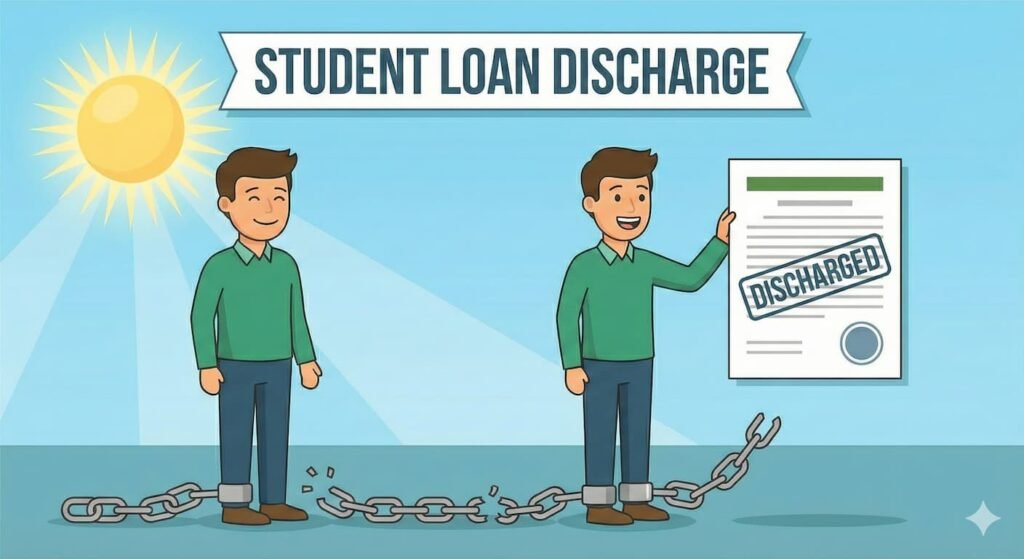

Why Wait?

The updated guidelines are a window of opportunity. As mentioned in the video, this process could potentially clear your stress and hassle in as little as three to six months.

This isn’t just about money; it’s about freedom. It’s about finally getting that “bad ex” out of your life permanently.

Want the Step-by-Step Blueprint?

I have done the research so you don’t have to. I wrote the book “Discharge Student Loan Debt in a Bankruptcy” to walk you through exactly how to take advantage of these new laws.

Don’t let the application process scare you. If 87% of people are succeeding, why aren’t you doing this?